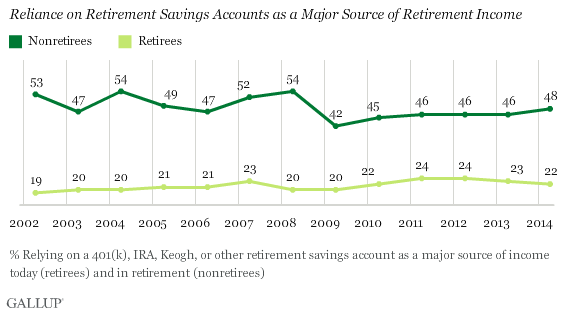

WASHINGTON, D.C. -- Prior to the Great Recession, most Americans planned to rely on a 401(k), IRA, Keogh, or other retirement savings account when they retire. Today, 48% of Americans say they would rely on a 401(k) account in retirement -- a percentage that (48%) has not rebounded to pre-recession levels.

In April 2008, 54% of Americans who had yet to retire expected to rely on a 401(k) as a major source of income. This dropped to 42% in 2009, in the depths of the recession, but has been rebounding ever since.

During the recession, many working Americans saw the value of their 401(k) accounts drop, which may have made them skeptical that they would be able to rely on these accounts as a source of retirement income. Stocks and 401(k) accounts have recovered much of their value since then, and simultaneously, the percentage of nonretired Americans who plan to use these retirement accounts as a source of income has increased.

The percentage of nonretired Americans who plan to rely on a 401(k) is far higher than the percentage of retired Americans who do rely on a 401(k) or other retirement savings account, currently 22%. The recession did not affect retired Americans' reliance on 401(k)s and other retirement savings accounts as much as it affected nonretirees' projected reliance on these accounts.

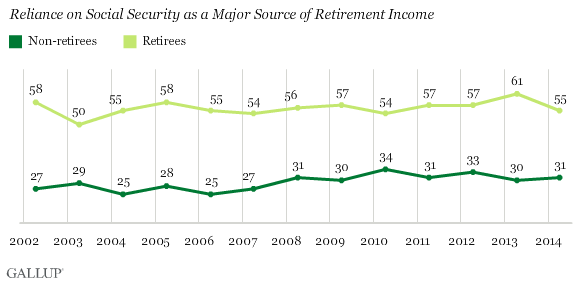

The Role of Social Security in Retirement Income

Historically, Social Security has been more of a prominent factor in the incomes of retired Americans than in the retirement plans of nonretired Americans. Over the 12 years Gallup has been tracking this measure, between 50% and 61% of retirees have considered Social Security a major source of income. By contrast, between 25% and 34% of nonretirees have expected it to be a major income source when they reach retirement.

Since the recession began, more nonretirees have expected Social Security to be a major source of retirement income than did so before 2008. From 2002 to 2007, between 25% and 29% of nonretirees expected it to be a major source of income, compared with 30% to 34% from 2008 to 2014. This may reflect the higher volatility in the stock and housing markets, as fewer Americans felt comfortable trusting their retirement income to these sources and instead considered Social Security the safer option.

However, an additional 51% of nonretired Americans do expect to rely on Social Security as a minor source of income. So while nonretired Americans mostly don't expect to rely on it as a major source of income, most expect it to fund their retirement to some degree -- not a surprising finding, given that Social Security is currently guaranteed for most working Americans.

Implications

For many Americans, saving for retirement is a scary prospect. It is the top financial worry for 59% of Americans. Already-retired Americans largely use sources that are outside of their control, like Social Security and employer-sponsored pension plans, as a source of income. But Americans who are still working toward retirement generally expect 401(k) accounts, IRAs, CDs, and other savings accounts to be major sources of retirement funds. Americans generally have more control over these types of savings plans, in terms of how much money they contribute and where that money is saved or invested. Still, this could be problematic because of studies showing how few workers today have adequately built up their savings to the point at which they can actually rely on them in retirement.

A recent Wells Fargo/Gallup Investor and Retirement Optimism survey found that investors are generally risk-averse when it comes to retirement savings, favoring security over larger growth potential. This could influence the amount today's working Americans have saved when they approach their desired retirement age.

Time will tell if this switch to self-controlled retirement savings plans is successful for working Americans. One-third of nonretirees still plan to rely on Social Security as a major income source, and half plan to rely on Social Security as a minor source. But there may be looming problems for Social Security system, because the 65-and-older population is essentially going to double in the years ahead as the huge group of baby boomers move into their later years. Many baby boomers are reluctant to retire, whether because they enjoy working or because they can't afford to. It is worth monitoring how their plans change when these baby boomers eventually decide to stop working and retire.

Survey Methods

Results for this Gallup poll are based on telephone interviews conducted April 3-6, 2014, with a random sample of 1,026 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia.

For results based on the total sample of national adults, the margin of sampling error is ±4 percentage points at the 95% confidence level.

For results based on the sample of 334 retirees, the margin of sampling error is ±7 percentage points at the 95% confidence level.

For results based on the sample of 692 nonretirees, the margin of sampling error is ±5 percentage points at the 95% confidence level.

Interviews are conducted with respondents on landline telephones and cellular phones, with interviews conducted in Spanish for respondents who are primarily Spanish-speaking. Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods. Landline respondents are chosen at random within each household on the basis of which member had the most recent birthday.

Samples are weighted to correct for unequal selection probability, nonresponse, and double coverage of landline and cell users in the two sampling frames. They are also weighted to match the national demographics of gender, age, race, Hispanic ethnicity, education, region, population density, and phone status (cellphone only/landline only/both, and cellphone mostly). Demographic weighting targets are based on the most recent Current Population Survey figures for the aged 18 and older U.S. population. Phone status targets are based on the most recent National Health Interview Survey. Population density targets are based on the most recent U.S. census. All reported margins of sampling error include the computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

View survey methodology, complete question responses, and trends.

For more details on Gallup's polling methodology, visit www.gallup.com.