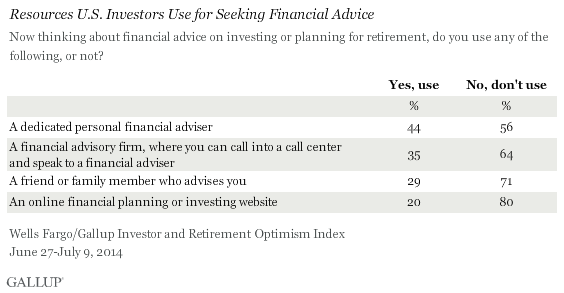

PRINCETON, NJ -- Even as access to the Internet has become ubiquitous in the U.S. and data analytics is highly touted for use in finance, U.S. investors are more likely to have a dedicated financial adviser than to use a financial website for obtaining advice on investing or planning for their retirement, 44% vs. 20%.

More investors also report using either a financial advisory firm that gives them access to live advice through a call center (35%) or a friend or family member (29%) to advise them than using a financial website.

These findings are based on a Wells Fargo/Gallup Investor and Retirement Optimism Index survey conducted in late June and early July. The survey is based on a nationally representative sample of U.S. investors with $10,000 or more in stocks, bonds, mutual funds, or in a self-directed IRA or 401(k).

Retirees, High-Value Investors Gravitate Toward Dedicated Financial Advisers

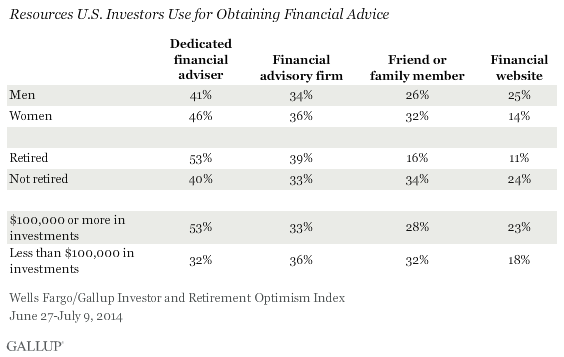

Among U.S. investors, retirees and investors with $100,000 or more in invested assets are significantly more likely than their counterparts to use a dedicated financial adviser. Nonretirees are more likely than retirees to use financial websites or to rely on friends and family.

Men and women are about equally likely to report using three of the four advice resources. The exception is financial websites, which men are about twice as likely as women to say they use, 25% vs. 14%. There is little difference across types of investors in the use of financial advisory firms, with about a third of each demographic group saying they use one.

Eight in 10 Investors Receive Advice Somewhere

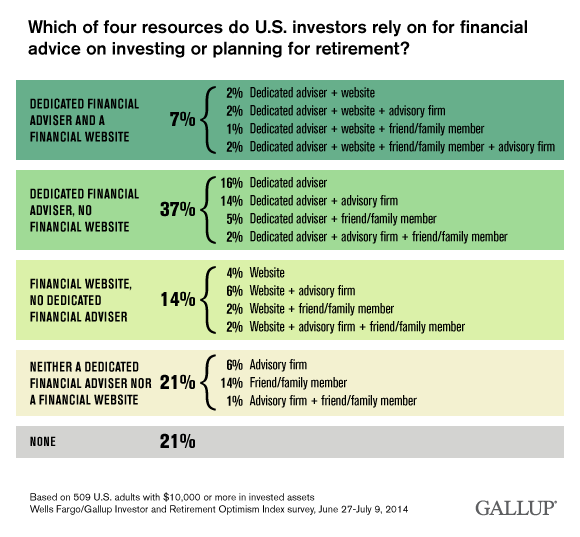

Overall, 79% of investors report using at least one of the four financial advice resources tested, while 21% don't use any of the four. The largest percentage of investors -- 40% -- rely on just one source, but almost a third (30%) rely on two, 7% on three, and 2% on all four.

The following chart details how investors fall into all 16 possible combinations of the four resources. Of particular note is that many more investors rely on a financial adviser to the exclusion of a financial website than the reverse: 37% vs. 14%. Only 7% rely on both, either alone or in combination with other resources.

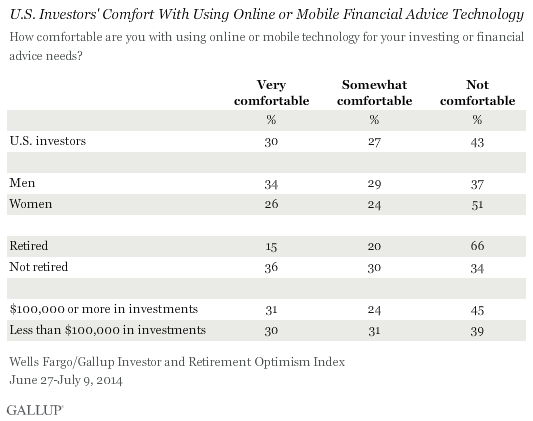

Part of what may be suppressing investors' use of online financial resources is that less than a third of investors -- 30% -- say they are "very comfortable" using online or mobile technology for their investing or financial advice needs. While another 27% are somewhat comfortable, 43% say they are not comfortable with this.

There is a strong generational skew in these attitudes, with 66% of nonretirees indicating at least some level of comfort with online financial advice tools, compared with 35% of retirees. Additionally, men have a higher comfort level than women. (More details are shown on page 2.)

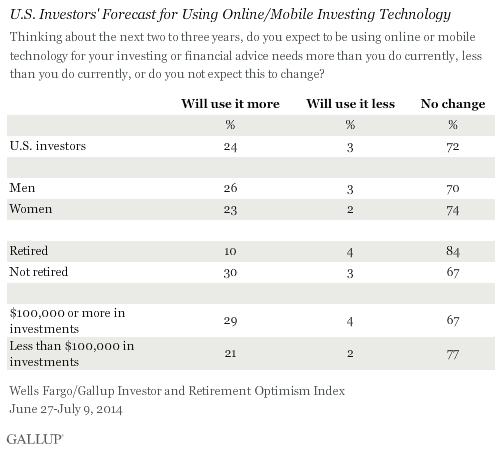

And while people may not always be the best judge of their own likelihood of adopting technology in the future, just one in four investors -- 24% -- say they expect to use online or mobile technology more in the next two to three years than they do currently. (See page 2 for demographic breaks.)

Implications

The most recent Wells Fargo/Gallup survey shows that the great majority of investors feel they need expert advice to help them invest in the stock market, and the desire for professional input would likely be greater when advice needed for other types of financial matters (such as planning for retirement, college expenses, and healthcare) is factored in. Accordingly, eight in 10 investors report that they do receive advice in some form, spanning the four sources of advice tested in the poll. And despite lots of buzz about online financial tools that allow users to submit their portfolios to computer algorithms, most investors still feel more comfortable involving a human, whether in the form of a dedicated personal adviser or a financial advisory firm that gives them access to live counselors in a call center.

This shouldn't be an either-or situation. Investors who want the best of both worlds can probably get it by seeking a partnership with financial advisers who are tapping into the same powerful analysis tools being offered to consumers online. In fact, such a marriage of humans and computers could be a strong selling point for the financial services industry -- bridging consumers' reluctance to go it alone online with their desire for a human connection and the best possible performance for their investments.

Survey Methods

These findings are part of the Wells Fargo-Gallup Investor and Retirement Optimism Index, which was conducted June 27-July 9, 2014, by telephone. The sample for the Index included 1,036 investors, aged 18 and older, living in all 50 states and the District of Columbia. For this study, the American investor is defined as any person or spouse in a household with total savings and investments of $10,000 or more. About two in five American households have at least $10,000 in savings and investments in stocks, bonds, mutual funds, or in a self-directed IRA or 401(k). The sample consists of 72% nonretired investors and 28% retired investors.

Questions about how investors get financial advice were asked of a random half-sample of 509 U.S. investors. The margin of sampling error for these results is ±5 percentage points at the 95% confidence level.

Interviews are conducted with respondents on landline telephones and cellular phones, with interviews conducted in Spanish for respondents who are primarily Spanish-speaking. Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods. Landline respondents are chosen at random within each household on the basis of which member had the most recent birthday.

Samples are weighted to correct for unequal selection probability, nonresponse, and double coverage of landline and cell users in the two sampling frames. They are also weighted to match the national demographics of gender, age, race, Hispanic ethnicity, education, region, population density, and phone status (cellphone only/landline only/both, and cellphone mostly). Demographic weighting targets are based on the most recent Current Population Survey figures for the aged 18 and older U.S. population. Phone status targets are based on the most recent National Health Interview Survey. Population density targets are based on the most recent U.S. census. All reported margins of sampling error include the computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

For more details on Gallup's polling methodology, visit www.gallup.com.