Story Highlights

- Low customer confidence puts the industry at risk for regulation

- When customers trust their bank, they tend to trust the banking industry

- Some banks are eroding public trust, while others are building it

If banks are serious about rebuilding consumer trust, they need to get their own houses in order.

The good news: banks have seen a year-over-year gain in trust.

Consumers' confidence in banks increased in 2017.

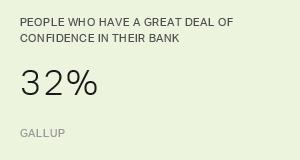

But still, only 32% of people have "a great deal" or "quite a lot" of confidence in banks.

This is a five-percentage-point increase from 2016, and an 11-point increase from the 38-year low recorded during the Great Recession.

However, the current level is relatively low for banks, historically, and below the average confidence level for all institutions.

Some banks inspire more confidence; some cause more doubt.

There is a tremendous amount of variation in industry trust depending on a customer's primary bank.

Our Gallup Retail Banking study showed an industry-low level of 18% confidence in banks at one financial institution, and a high of 48% confidence at another.

The banks that create high levels of confidence in the overall industry also tend to have much higher levels of customer engagement.

Engagement is a primary driver for industry confidence.

Customer engagement is Gallup's metric for the psychological and emotional attachment customers have to a company.

If a customer is fully engaged in their relationship with their bank, they are nearly four times more likely to have confidence in the banking industry compared with actively disengaged customers (customers who are resentful that their needs aren't being met and who are acting out their unhappiness).

This means, to a large degree, that how a customer feels about their bank is likely how they feel about the whole industry. Customers do not tend to love their primary bank, but say they "hate banks," or vice versa.

In many ways, banks are either their own worst enemy, or their own best ally, when it comes to creating confidence in the industry.

When there is low confidence, there can be greater risk for regulation.

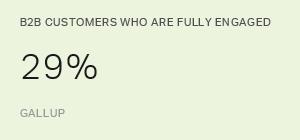

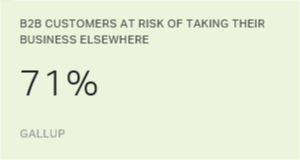

According to Gallup's most recent banking industry study, only 36% of banking customers are fully engaged.

Best in class is 71%, while the industry low is 13%.

This extreme variation clearly indicates that the industry as a whole has significant opportunities to engage their customers and continue to increase overall confidence.

It also means that some banks are creating much higher (or lower) levels of industry confidence than others.

So whose interests really matter?

Whether or not customers believe their bank has their best interests at heart is a strong indicator of engagement.

Our annual banking study showed only 12% of customers at one bank were extremely satisfied that their bank had their best interests at heart, while another bank led the industry with 64% of customers feeling extremely satisfied.

The No. 1 way banks can show customers that their interests are ahead of the bank's own? Helping improve a customer's financial well-being.

Customers want their bank/banker to help them:

- See their financial potential

- Understand how their needs may change over time

- See how the specific products or services integrate with their lifestyle

Industry confidence goes beyond primary bank engagement.

While customers feel more confident in the industry when they're engaged with their primary bank, there are certainly other factors at play.

One bank's actions can create collateral damage that extends to the entire industry.

Our advice is that individual banks and the industry as a whole, should commit to, and hold each other accountable for:

- Creating a proactive culture of compliance (with benchmarks and predictive indicators)

- Benchmarking and aligning their culture, practices and policies to improve customers' financial well-being

- Publicly owning up to mistakes

- Correcting problems both local and systemic the first time -- even beyond what customers may expect

- Committing to radical transparency and simplicity with fees, terms and policies

- Safeguarding customers' identities and data

The industry should demonstrate it is serious about public confidence and holding itself to a high bar by:

- establishing clear minimum standards of performance

- having clear accountability and resolution steps for banks that do not meet the thresholds

Establishing a dedicated governing body -- similar to bar associations or medical boards -- may also inspire more confidence among U.S. adults.

Another option is for industry groups, such as the Consumer Bankers Association, Bank Administration Institute and American Bankers Association, to form a governing coalition with oversight authority.

In doing so, the banking industry would send a clear message to regulators and the public that it is willing to take an honest look in the mirror and get its own house in order.

Engage your customers to foster loyalty and increase trust in your bank.