Story Highlights

- Millennials are the least engaged generation when it comes to their primary bank

- They have more banking problems and switch banks more often than other generations

- Banks can use data-driven decision-making to appeal to their millennial customers

Millennials now surpass baby boomers as the largest generation in the U.S. -- 73 million strong according to Gallup's 2016 estimates.

An estimated $30 trillion in wealth will transfer from baby boomers to millennials over the next 30 years.

Although previous myths about millennials not being valuable customers have been disproven, significant challenges remain for retail banking leaders who want to engage the millennial banking segment.

Gallup analytics show that millennials in the U.S. have the lowest levels of customer engagement (only 25% are fully engaged) across multiple industries.

We've found that these generational trends apply to the retail banking industry, too.

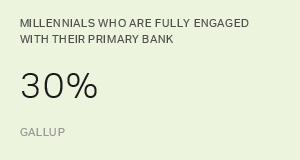

Indeed, Gallup's most recent retail banking study once again demonstrated that millennials have the lowest levels of customer engagement with their primary retail bank (30% are fully engaged) compared with baby boomers (40%) and traditionalists (51%).

Based on these data, it is not surprising that millennial customers were also the most likely to switch their primary bank in the past year.

Millennial customers (8.4%) reported recently switching their primary bank at a rate that is about 2.5 times more often than baby boomers (3.6%) or traditionalists (3.3%) and 1.5 times more often than Gen Xers (5.5%).

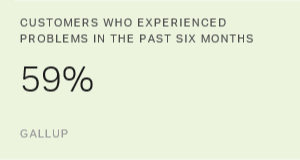

Given that customer disputes and problems can decimate customer engagement, we recently asked customers about problems they had with their primary bank in the past six months.

We hypothesized that millennial disengagement might be due to different experiences with their primary banks when they have problems.

We found that millennials were slightly more likely to say they had a problem (13%) compared with baby boomers (10%) or traditionalists (7%).

However, millennials were the least likely generation to report the problem to their bank when they had one.

More importantly, among those who did report the problem, only two in 10 millennials were extremely satisfied with their problem resolution compared with three in 10 baby boomers and half of traditionalists.

So what can banks do in the face of these discerning millennial customers?

1. Predict their problems.

Because millennials are less likely to report problems, you need better systems for predicting, tracking and solving customer problems.

You should closely monitor indicators of potential customer problems and address them proactively.

For instance, do you know what customer behaviors predict overdrafting and unnecessary fees?

If so, are you warning your customers about these potential consequences?

For instance, one national bank offers credit score monitoring with instant mobile alerts when customers' credit scores change.

Other financial institutions have increasingly relied on mobile notifications of suspicious account activity, such as unusual spending activity or locations.

2. Help them speak up.

You should make it easier to report a problem, so customers don't have to physically walk into a branch or call a bank representative to settle their concerns.

The ability to report problems via multiple banking channels, such as a mobile app, automated phone line, text, email or instant message can help -- but only if customers do not have to repeat their information multiple times.

You can also proactively use pulse surveys to hear customer concerns and experiences.

3. Forgive a few fees.

Millennials were most likely to leave their primary bank because of account fees and service charges.

Some national banks charge up to $35 per overdraft, while newer fintech companies -- digital technology firms that enable financial transactions -- now offer zero-fee options for checking and savings accounts.

It might be more beneficial to overlook a few service charges when considering the long-term relationship with these customers and growing millennial wealth.

4. Differentiate their banking experience.

It is critical that retail banks understand and segment customer interactions.

You should create customer journey and data maps to establish an omnichannel framework for all customer experiences.

By attaching data -- both customer perceptions and behaviors -- to each touchpoint of a customer interaction, banking leaders can take a more data-based approach in reacting to and adjusting their services to meet consumer needs and behaviors.

In Part 2 of our series, we explore how millennials interact with their primary bank in contrast with previous generations and advise retail banks on how to make the most of those interactions.

- Download our free report to learn how millennials are changing the economic landscape permanently.

- Engage your millennial banking customers to prevent losing them to your competitors.

- Learn more about how to improve business outcomes using customer engagement.

Learn more about how the Gallup Panel works.